In 1981, Kodak, the historic camera maker, enjoyed $10 bn in sales. In 2004, Blockbuster boasted of its 9,000-strong video store footprint. Today, these one-time giants have all but disappeared.

The moral of their downfall usually focuses on a failure to predict the competition. But that’s the wrong lesson to draw. When Kodak filed for bankruptcy in 2012, it wasn’t because management didn’t foresee an alternative to film photography: the digital camera was invented by a Kodak engineer in 1975.

And Blockbuster didn’t cease operations in 2013 because it failed to notice the competition. CEO John Antioco was offered the opportunity to buy Netflix for $50 mn in 2000. He passed on the deal because he assumed Netflix would never amount to more than a niche player (it’s worth $222 bn today).

The leadership of both companies ultimately suffered from a failure of imagination. The prospect of new competition was well understood but management was too beholden to the status quo and couldn’t conceive of a future different from the present.

This is where a materiality assessment can help. The process attempts to reveal the big picture by scanning the horizon for the big ESG risks and opportunities ahead, before linking these issues to an organization’s core value proposition.

Both science and art, a good materiality assessment is rigorous in researching, recording and prioritizing any topic that might be relevant (ie, material), but imaginative enough to explain how those issues could affect the sector and company in question.

Think of financial materiality

The concept of materiality comes from financial reporting, where auditors are allowed to use their professional judgment on whether the omission or misstatement of information is likely to significantly influence the decision of a reasonable investor. If an investor would have likely changed its actions if the information had not been omitted or misstated, then it is considered to be material.

Materiality in relation to sustainability follows the same logic. A company’s sustainability disclosure should include information likely to significantly influence the views of stakeholders by clearly identifying and prioritizing the topics that matter most, rather than addressing at length every ESG consideration a company might face. If an ESG issue is important enough to be disclosed to stakeholders, it should also be reflected in the organization’s strategy.

Benefits

Conducting a materiality assessment before you create and communicate a sustainability strategy delivers a number of benefits:

- It helps clarify the ESG risks and opportunities ahead. As mentioned, a good assessment will uncover risks and opportunities not readily apparent on the balance sheet. While mitigating risk is an obvious benefit, finding opportunities can be even more valuable. The generation of a single valuable idea via stakeholder engagement or research can generate a substantial return on investment

- It responds to stakeholder expectations. Many stakeholders, particularly investors, want to understand which sustainability issues are most important to a business. The assessment process gives a clear framework to help you align company efforts and resources with their expectations

- It provides the structure for a focused annual, sustainability or integrated report. By identifying and prioritizing the sustainability topics most relevant to a company, a materiality assessment allows you to draft a more focused report, which is more likely to be read

- It increases the strategic value of sustainability. Sustainability can be seen by some as supplementary to the ‘real’ business of a company. A materiality assessment adds strategic weight to a sustainability agenda by connecting ESG issues to a business’ core value proposition. Done properly, a materiality assessment will also ensure the views of senior management are methodically reflected, ensuring buy-in across all areas of the organization.

Our understanding of materiality is now expanding on the basis that ESG risks and opportunities have financial consequences. This sounds obvious. But many risk, strategy and finance professionals continue to treat sustainability as a public affairs issue, rather than a driver of business value.

An international 2017 study, for example, found a staggering 35 percent of companies had no alignment between the risks deemed material in the sustainability report and the risks disclosed in their legal risk filings.

In truth, there should be no distinction between different kinds of risks and opportunities. Although often new and emerging, ESG issues are simply business risks and opportunities that should be considered, prioritized and, where appropriate, acted upon.

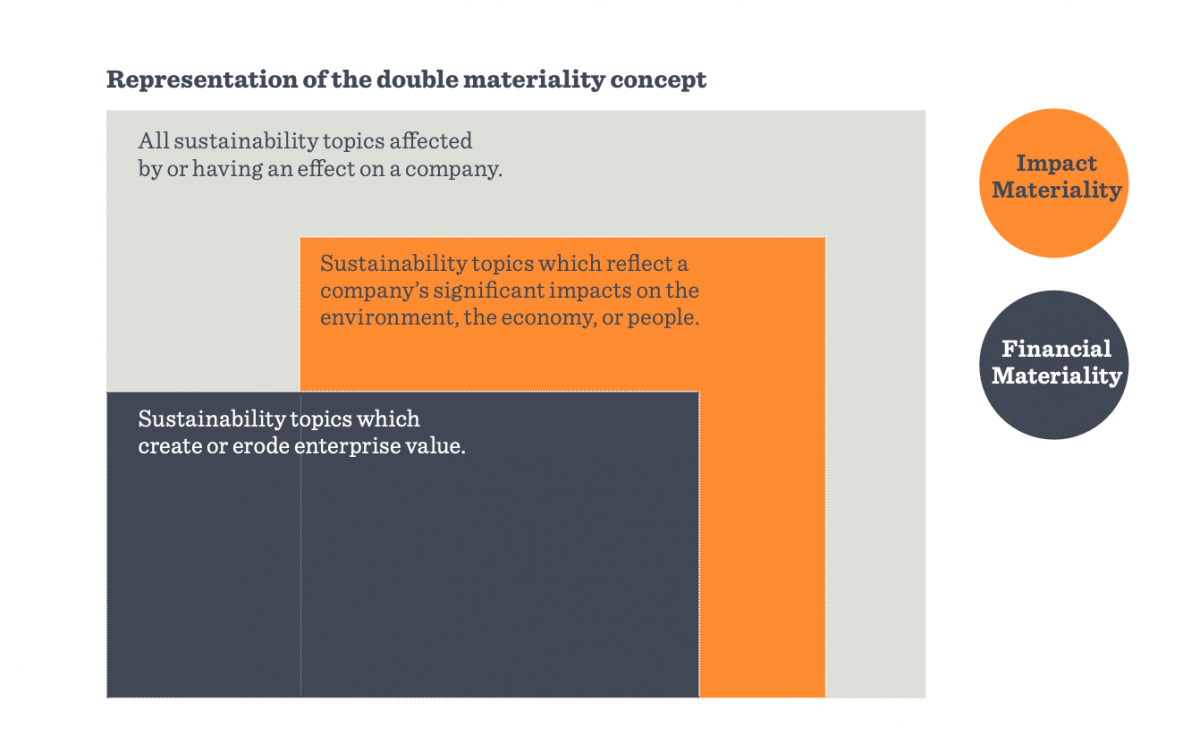

Double materiality

Enter double materiality (sometimes referred to as nested materiality), the best method yet devised for integrating ESG into a business’ core strategy and corporate reporting. Popularized by a report from the big five reporting standards-setters in December 2020, and a subsequent report by the European Financial Reporting Advisory Group in February 2021, the concept explains that a materiality assessment should prioritize both:

- financially material topics, which create or erode enterprise value (a focus for investors). These topics also provide the structure for an integrated (annual) report

- ‘impact’ material topics, which reflect significant positive or negative impacts on people, the economy and the environment (a focus for a diverse range of stakeholders). These topics also provide the structure for a sustainability report.

The implementation of materiality into a company’s corporate strategy and disclosure has many benefits and, in our experience, delivers an outstanding return on investment.

Luke Heilbuth is head of strategy at BWD.

Luke Heilbuth

Luke Heilbuth is the CEO of BWD, a sustainability advisory firm with offices in New York and Sydney. By combining best practice sustainability strategy and reporting with original design and data visualisation, BWD cuts through the complexity of...